2026 Benchmark Hub

We’ve assessed 2,000 of the world’s most influential companies, ranking and measuring them on their impact on people and planet

The state of global corporate accountability.

The 2,000 companies included in this analysis, generate USD 53 trillion in revenues and account for 54% of global emissions. They directly employ 107 million people and support a further 550 million livelihoods through their value and supply chains. Their collective power is undisputed − their decisions can help drive climate solutions, restore nature, and ensure prosperity for all.

The data makes one reality unmistakably clear: the pathway to a sustainable future depends on business playing a central role in driving global systems change. Proven solutions, effective mechanisms, and growing momentum already exist among some leading companies, yet too many continue to fall behind. Companies face a clear choice, and decisive action and scaled investment from the world’s most powerful and influential businesses are now urgent.

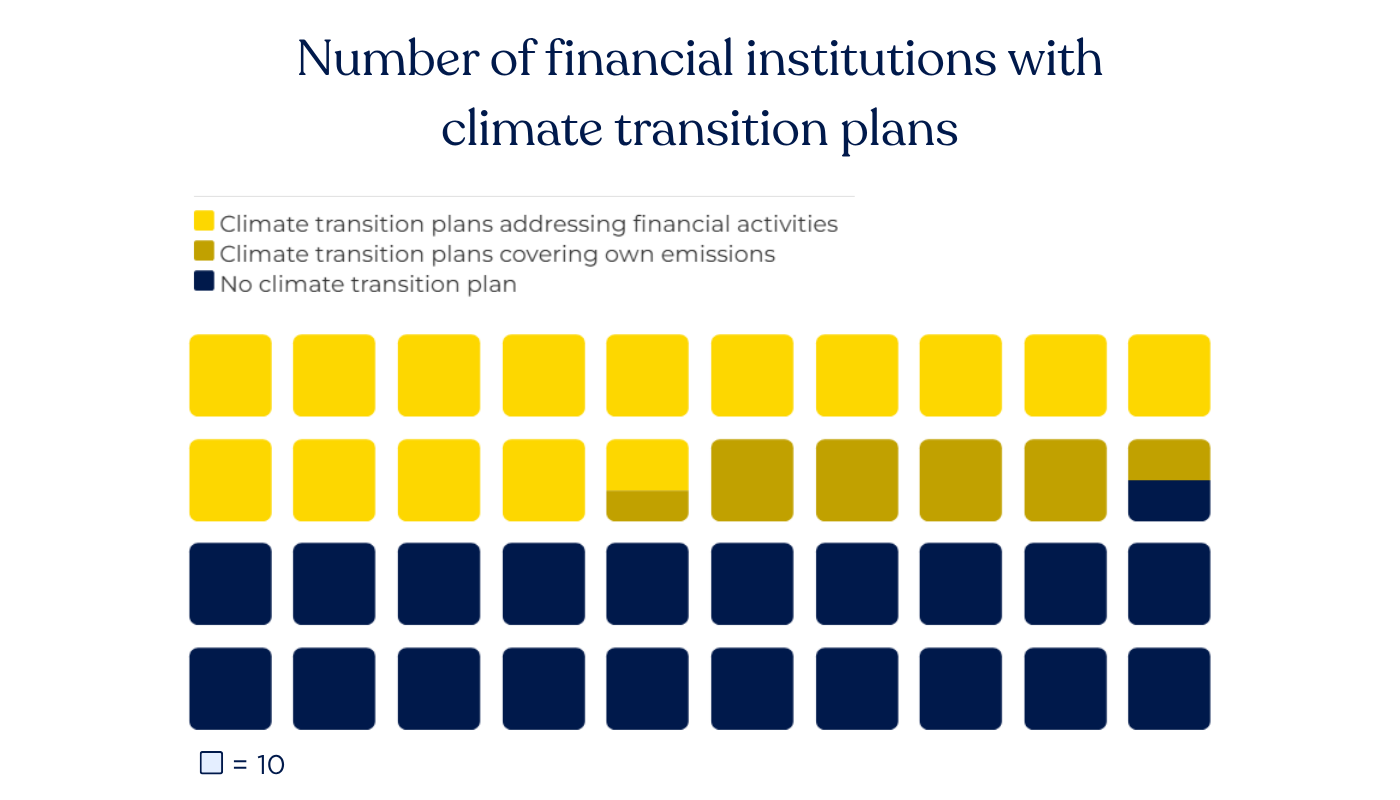

The global financial system is beginning to build the architecture for transition planning, with over 36% of the 400 financial institutions assessed publishing plans covering financing activities. However, major gaps remain, with more than half still lacking even basic transition planning.

Read more

Up to 30% of the annual clean-energy investment gap needed by 2030 could be closed if companies scaled investment to levels already proven in the market and observed across sectors, moving the world closer to a 1.5°C-aligned pathway

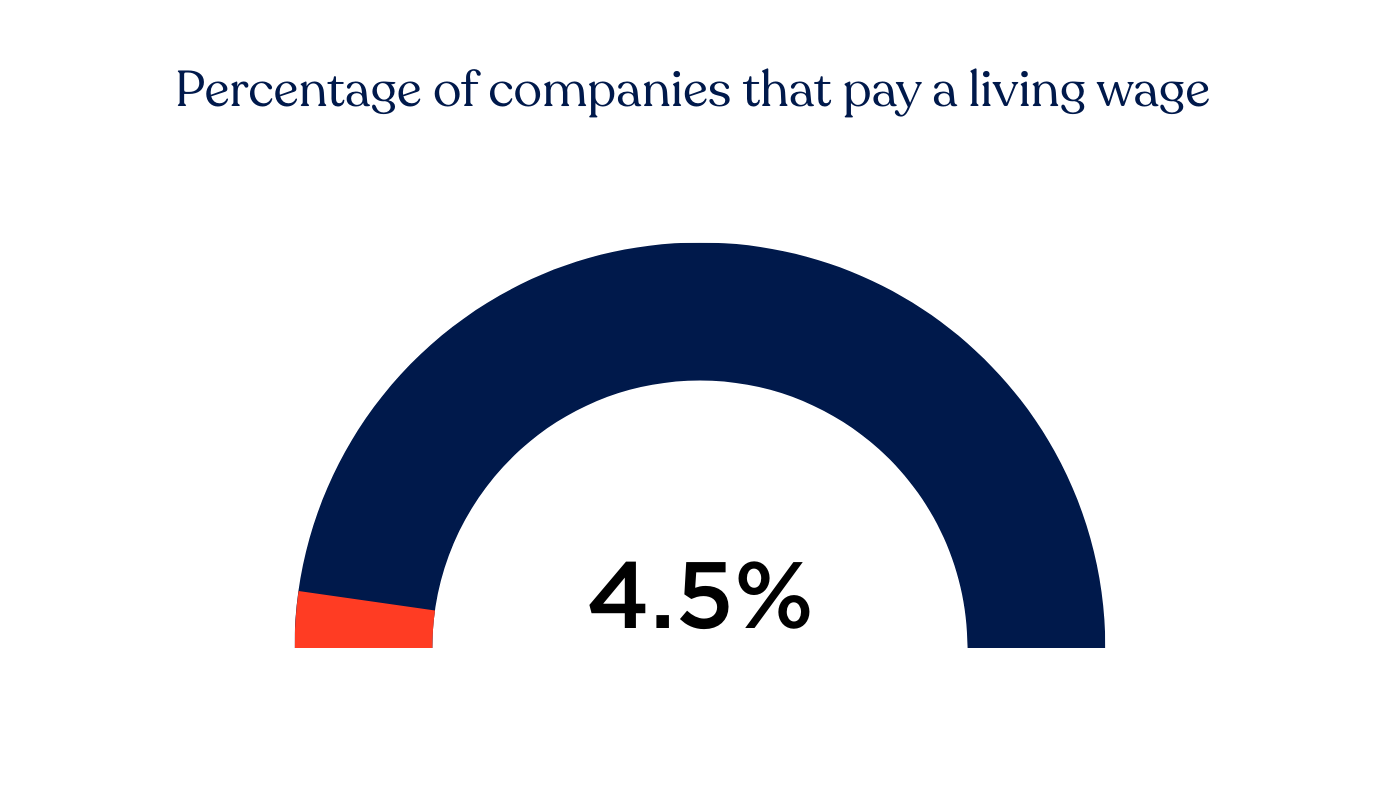

Read moreLess than 5% of major companies pay a living wage, leaving households worldwide under growing financial strain

Read more

So far only 9% of companies quantify their nature-related risks, leaving the path wide open for early movers.

Read more

10% of companies assess human rights risks in their supply chain, while only one in five trace their products to understand nature impacts

Read more

While 38% of major tech companies publish their ethical AI principles, none of them disclose their human rights impact assessment results, exposing weak accountability across the sector

Read more

About 2026 benchmarks

Our new research marks the first time 2,000 companies have been assessed simultaneously across seven systems transformations. It draws on insights and evidence from seven years of prior research across individual industries and sustainability topics.

The benchmarks include rankings, assessments, individual company scorecards and key performance data drawn from hundreds of indicators that measure how companies impact people and the planet. For each benchmark, we publish a methodology grounded in stakeholder expectations, current company practices, and global agendas.

Social

Our work is built around four complementary assessments that together evaluate corporate performance on key social and human rights issues. The Social Benchmark assesses 2,000 of the world’s most influential companies against 18 Core Social Indicators, embedding responsible business expectations across all assessments. The Corporate Human Rights Benchmark (CHRB) provides a deeper, sector-specific analysis of around 100 companies operating in high-risk sectors. The Gender Benchmark delivers an in-depth assessment of 100 companies in the apparel and food and agriculture sectors, while the Gender Assessment applies a streamlined set of gender indicators to all 2,000 companies, offering a scalable and comparable view of performance on gender equality.

Social Benchmark

We assess the 2,000 most influential companies on their performance on 18 core social indicators (CSIs). Given that the societal expectations reflected in these indicators are an integral part of responsible business conduct, CSI assessments are embedded into all of our benchmarks, representing 20% of the possible overall score. The 2,000 assessments combined are the basis for our Social Benchmark.

Corporate Human Rights Benchmark

The CHRB assesses around 100 companies operating in five high-risk sectors - food and agricultural products, apparel, extractives, ICT manufacturing and automotive manufacturing. The companies are scored across five measurement areas, each containing a series of indicators focusing on different aspects of how a business seeks to respect human rights in its own operations and supply chain.

Gender Benchmark

The Gender Benchmark assesses around 100 companies from two sectors that have been identified as having a great impact, both positive and negative, on gender equality: apparel, and food and agriculture. The companies have been scored on 91 elements across the measurement areas of governance and strategy, representation, compensation and benefits, health and well-being, violence and harassment, and marketplace and community.

Gender Assessment

The Gender Assessment applies a reduced set of Gender Benchmark Methodology indicators to all 2,000 companies. In total, we assessed them on 51 elements across five measurement areas: governance and strategy, representation, compensation and benefits, health and wellbeing, and violence and harassment.

Climate

We assess the most influential companies on the credibility and integrity of their transition plan, including their efforts to ensure that people, communities and other affected stakeholders are not left behind.

The Act Core assessment evaluates companies on the credibility and integrity of their transition plan, while the Just Transition assessment examines how they incorporate social equity, inclusivity, and workers’ rights into their strategy.

ACT Core

2,000 companies across multiple industries and sectors are assessed on their transition plan credibility along six measurement areas; emissions reporting and target definition, planning for the low-carbon transition, governance and policy, low-carbon investments, current target alignment, and performance.

Just Transition

2,000 companies across multiple industries and sectors are assessed on how they integrate social equity, inclusivity and the rights of workers into their transition plan, using three indicators: Fundamentals of social dialogue and stakeholder engagement in a just transition, Fundamentals of just transition planning, Fundamentals of decent work, workers and skills for a just transition.

Nature

Nature Benchmark

The Nature Benchmark assesses 750 companies across high-impact industries, from those directly managing natural resources like food, mining, and forestry, to those relying on resources further down the value chain, such as apparel, packaging, and pharmaceuticals. The Nature Benchmark has 18 nature-specific indicators and 18 Core Social Indicators. These indicators are split across four measurement areas: Governance, Planet, People and Core social indicators.

Ocean Benchmark

The 125 companies selected for assessment in the Ocean Benchmark are part of the 750 companies assessed in the Nature Benchmark. The companies spread across a wide range of industries, including seafood, maritime transport, offshore wind energy, shipbuilding, port operation, apparel, chemicals and more. The Ocean Benchmark has 47 indicators that are split across four measurement areas: Governance, Ecosystems and biodiversity, Social responsibility, and Core Social Indicators.

Digital

Digital Inclusion Benchmark

The Digital Inclusion Benchmark assesses 200 of the world's most influential digital technology companies on 15 indicators across five digital inclusion measurement areas: access, skills, use, innovation and sustainable value creation. In addition, it assesses companies on 18 core social indicators.

Ranking Digital Rights Index

We evaluate 14 of the world’s most powerful tech giants and 12 telecommunications companies on 37 indicators across three measurement areas: Governance, freedom of expression and information, and privacy.

Food and Agriculture

Food and Agriculture Benchmark

The 350 companies assessed in the benchmark span the entirety of the food and agriculture value chain: agricultural inputs, agricultural products and commodities, animal proteins, manufacturing and processing, retail and food service segments. The Food and Agriculture Benchmark has 23 food and agriculture-specific indicators and 18 core social indicators. These indicators are split across four measurement areas: Healthy food systems, Sustainable food systems, Inclusive food systems and Governance.

Urban

Urban Benchmark

WBA’s Urban Benchmark ranks the sustainability performance of the 300 most influential companies shaping urban environments worldwide, across sectors such as construction, energy, real estate, transport, waste and water management. The benchmark assesses how effectively the private sector is addressing essential urban needs while respecting planetary boundaries. It evaluates companies on several dimensions, such as decent work and human rights practices, environmental and climate impacts, social inclusion and overall sustainability leadership.

Latest updates

Subscribe to stay informed on our work

Keep up to date with all the latest from World Benchmarking Alliance