Financial institutions failing to back low-carbon economy amid fossil fuel crises

The World Benchmarking Alliance (WBA) has today released its latest Financial System Climate Assessment, showing the urgent need for 400 of the world’s most influential financial institutions to accelerate the shift of capital towards a low-carbon economy as repeated fossil fuel crises continue to expose them to economic and financial instability.

While over one third of the assessed financial institutions have initial signs of transition planning towards a low-carbon economy, major gaps remain in the credibility of their plans. Only two out of 400 companies have robust commitments to phase out fossil fuels – a step companies must take to demonstrate credible transition strategies and address escalating energy risks.

Assessing major companies across the financial sector, including banks, insurers, asset managers and asset owners such as Allianz, BlackRock and HSBC, the WBA analysis highlights the opportunity for stronger governance, clearer targets and credible transition planning.

Transition planning is gaining momentum but critical gaps persist

Over one third (146) of the 400 financial institutions assessed are setting metrics and targets to drive and monitor progress, or embedding transition planning within governance structures. However, when plans are judged on whether they cover financed activities – not just institutions’ own operations – only 26% meet this bar.

Credible transition plans require short‑term (by 2030) sectoral targets for financing low‑carbon solutions aligned with a 1.5°C pathway. Among institutions with transition plans, around a quarter (47 companies) have embedded one or more short‑term climate solutions financing targets that jointly align with the pathway.

The pattern varies by institution type: a fifth of banks’ transition plans include a time‑bound financing target aligned with 1.5°C, compared with less than 3% of asset managers; insurers and pension funds sit at 10% and 7% respectively. Banks are beginning to show what credible action looks like but progress across the wider financial system remains too limited to support an economy‑wide transition at pace.

Marginal fossil phase out plans are a bottleneck of plan credibility; only 2 have robust fossil fuel exit commitments

Only two financial institutions – ING and Zürcher Kantonalbank – demonstrate robust fossil fuel restrictions, including commitments to both phase out existing exposure and stop new financing flows.

This underscores a critical gap in the sector’s transition readiness: most institutions still lack comprehensive fossil fuel restrictions and credible strategies to manage the long-term transition risks associated with fossil fuel dependence, despite growing evidence that fossil fuel volatility poses wider economic and financial stability risks.

Pauliina Murphy, Engagement & Communications Director of the World Benchmarking Alliance, said:

"Repeated fossil fuel crises have starkly illustrated how vital transition planning is for global economic stability. Financial institutions are central to this; their decisions on allocating capital to low-carbon solutions and phasing out fossil fuels will determine how fast the global economy can rebuild its resilience. The building blocks for the 1.5°C pathway are increasingly in place as more institutions set plans and improve disclosure. The opportunity now is to link transition plans to capital allocation decisions and clear policy commitments to phase out fossil fuels. As expectations from regulators, markets and stakeholders continue to evolve, financial institutions that move early to strengthen credibility and transparency will be better positioned to benefit from the transition.”

Regional disparities remain amid limited disclosure on financed activities

Financial institutions with a transition plan are about eight times more likely to disclose the share of financed activities allocated to low-carbon solutions than those without one. Yet transparency across the sector remains limited: only 15% report financed fossil fuel activity, highlighting how far public disclosure still has to go. While there is evidence for different aspects of transition planning, none of the companies assessed demonstrate both sufficient ambition and sufficient reduction of their financed emissions, which results in consistently low scores across the assessment.

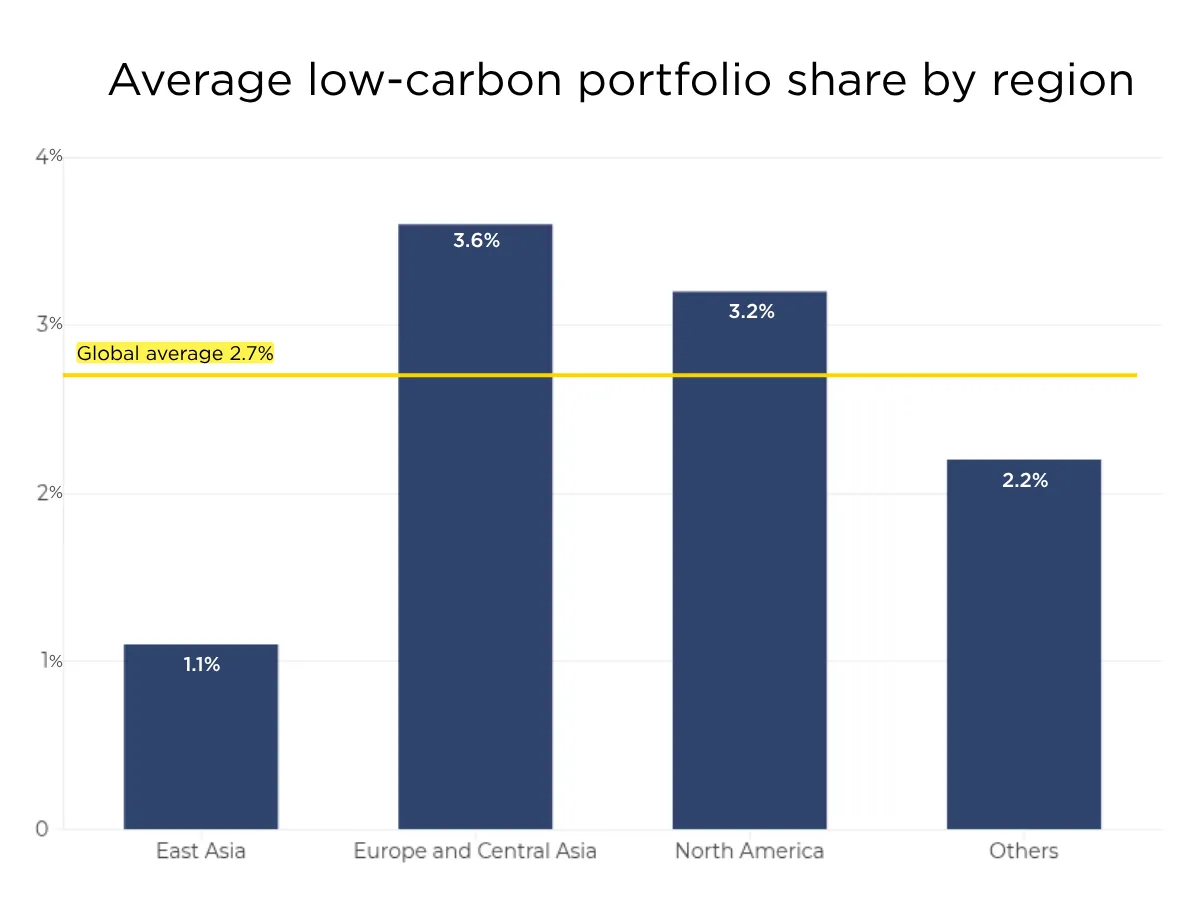

Despite the limitations of public disclosure, the assessment suggests that low-carbon activities represent on average a modest 2.7% of the total financed activities of the 400 financial institutions. Regional differences, however, are evident:

- Europe and Central Asia have the highest share of institutions with transition plans that cover financial activities (just over 60%). Its regional average share of disclosed low carbon financial activity is 3.6% of total activity, above the global average of 2.7%.

- North America has the lowest prevalence of transition plans among the regions highlighted (18%). Its average share of disclosed low carbon financial activity is 3.2%, broadly in line with the global average.

- East Asia has a low prevalence of plans (42%). Across Asia overall, institutions report the lowest average share of low carbon financial activity at around 1.1%, indicating the largest potential uplift.

Even the strongest-performing region – Europe and Central Asia – remains at only a few percentage points on low carbon financing disclosure, reinforcing the report’s overall conclusion that the financial system is still not reallocating capital towards low carbon solutions at the pace and scale required to support a resilient economic transition.

Subscribe to stay informed on our work

Keep up to date with all the latest from World Benchmarking Alliance